.png) The Kaizen Team

The Kaizen Team

How to Know If a Four-Day Workweek Is Right for Your Business

The four-day workweek has become one of the most talked-about workplace shifts of the last decade. Large corporations are experimenting with it....

Hiring an accounting firm is one of the smartest moves you can make for your business. But what actually happens behind the scenes each month, and what could you miss without it?

It’s easy to think of accounting as “tracking expenses” or “filing taxes”, but for businesses that work with us monthly, there’s a whole lot more going on. Your numbers aren’t just recorded. They’re reviewed, analyzed, and turned into decisions you can act on.

Let’s walk through what that looks like.

Before monthly accounting can give you useful insights, we need to make sure your systems and records are set up the right way. Onboarding is where we get to know your business and build the foundation for accurate, meaningful monthly reporting.

During onboarding, your firm will:

Learn about your business model, services, and operations.

Review your current financial processes and identify any gaps.

Teach you how to use any new tools or systems.

Clean up your books and reconcile historical records so you’re starting with accurate data.

Understand your goals, so we can help ensure your numbers support your plans.

The goal here isn’t just to “get set up.” It’s to understand your business well enough to give you relevant, strategic guidance from day one.

🔍 Want to see the full process? Check out our onboarding breakdown here.

Once onboarding is complete, your accounting team moves into a regular rhythm to keep your books accurate and up to date. Each month, we handle the behind-the-scenes work so your financial data is always reliable when you need it.

Here’s what this includes:

Accurate monthly maintenance means you’ll always have clean and trustworthy numbers. This gives you confidence when it’s time to talk strategy and make decisions.

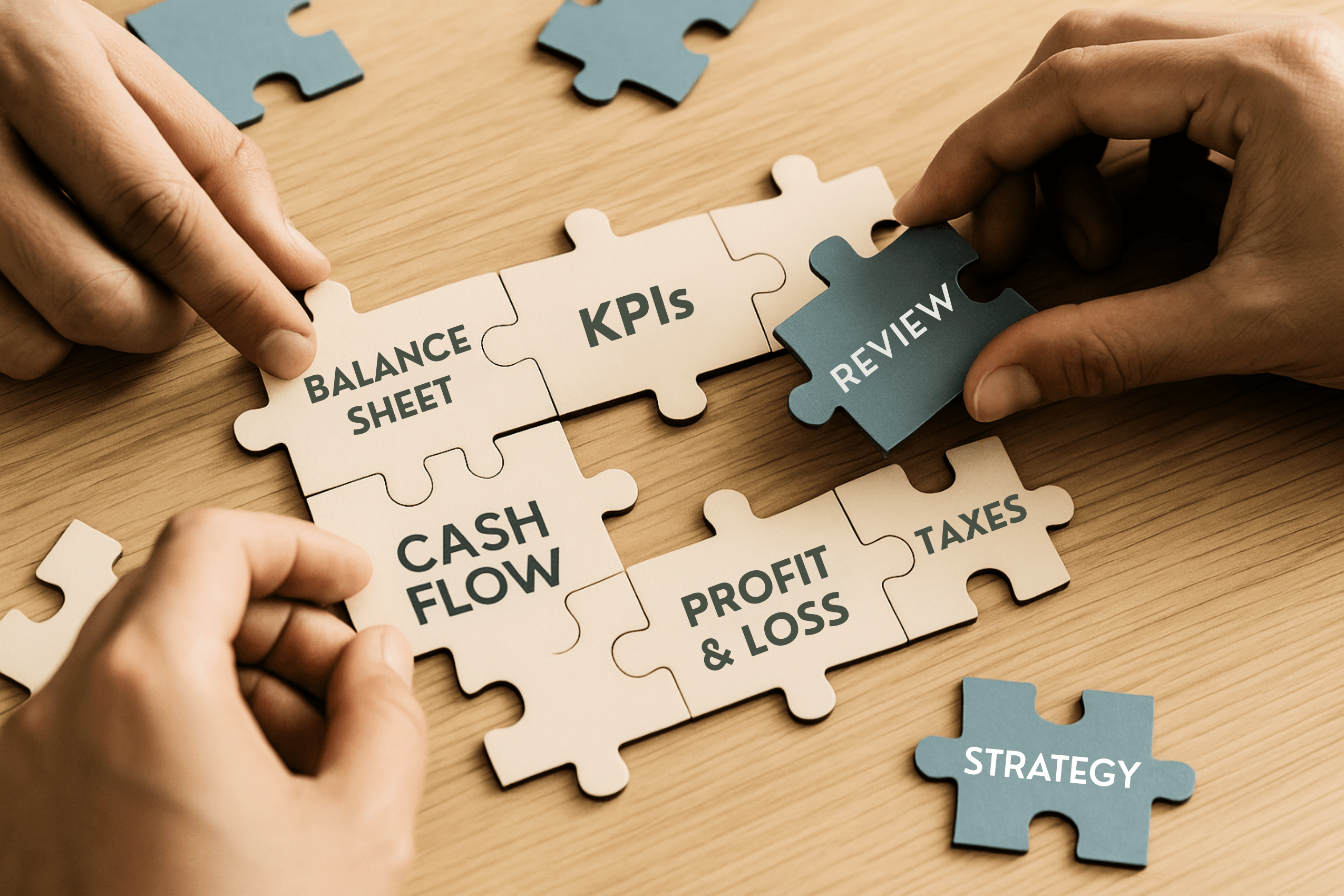

Each month, your accounting team organizes your financial data into accurate, easy-to-read reports. After reconciling your books and reviewing your transactions, they prepare a full reporting package so you have everything you have a clear, up-to-date picture of your business’s financial health.

The core reports typically include:

These reports don’t just sit in a folder. They are the foundation for your monthly review, where we interpret what the numbers actually mean for your business.

🔍 Related article: How to Read Your Financial Statements

Once your monthly reports are ready, your accounting team moves into review mode. This is where the numbers become more than data, and they start telling the story of your business’s performance and guiding decisions.

During the review, your accounting firm will:

Verify accuracy: Double-check the data to confirm that reports are based on facts, not assumptions.

Spot trends: Compare results month to month to identify shifts in revenue, expenses, and profitability.

Track progress: Measure how your performance stacks up against the goals you’ve set.

Provide insights: Highlight opportunities, potential issues, and adjustments you may want to consider.

If something needs your attention, such as rising expenses, a cash flow crunch, or a dip in revenue, you’ll know about it right away rather than months later.

🔍 Related article: What's In Your Balance Sheet and Why It Matters

Your monthly reports aren’t just numbers on a page. They show what’s working, what’s changing, and where action might be needed. With accurate, up-to-date financial data, your accounting firm helps you:

Identify growth opportunities: Adjust pricing, negotiate better vendor rates, or expand services where margins are strongest.

Catch potential problems early: Spot rising expenses, declining revenue, or slipping profit margins before they become bigger issues.

Plan ahead for cash flow: If reports show a slowdown coming, you can prepare before it impacts operations.

Make proactive tax decisions: Capture deductions and credits throughout the year so you’re not scrambling when tax time arrives.

Spotting these insights is just the first step. Next, we use them to make data-driven decisions about pricing, spending, and strategy.

🔍 Related video: Where Did My Money Go? Profit vs Cash Flow

Once we identify trends and risks, your monthly reports become a roadmap. This is where insights turn into actionable strategies to improve cash flow, strengthen margins, and guide long-term decisions.

Your accounting firm can help you:

Prioritize tax strategies: Capture deductions and credits throughout the year so you avoid scrambling at tax time.

Shift spending intentionally: Redirect resources toward what’s working and cut back where margins are thin.

Plan for pricing and growth: Use performance insights to guide decisions around pricing, staffing, or service expansion.

Run “what-if” scenarios: Model the financial impact of major decisions before you commit, whether it’s hiring, adding services, or preparing for slower seasons.

With these adjustments, your numbers stop being static reports and become active tools that drive better business decisions all year long.

Without ongoing accounting, you’re left guessing. And guessing can cost you.

If you wait until February to drop off your tax papers, you’ll have fewer options, less flexibility, and may even pay taxes you could have avoided with year-round planning.

Without a clear plan, the future of your business can feel uncertain and your goals harder to reach. That’s why we recommend moving to a monthly, ongoing relationship with an experienced accounting firm that will take a comprehensive approach to your business. They’ll give you a clear, focused picture of your business and a monthly plan for reaching your goals.

Are you thinking it’s time to get more clarity?

Let’s talk about how a monthly accounting partnership can give you clearer numbers, deeper insights, and the confidence to make smarter business decisions.

YPD HCM is part of the Kaizen CPAs family. YPD HCM specializes in payroll and HR compliance for small businesses, providing the hands-on support to get your people paid and stay compliant without having to become an expert yourself.

The information in this article is provided for general educational purposes and reflects conditions as of the publication date. It does not constitute legal, tax, or compliance advice. For guidance specific to your business, consult a qualified professional.

The four-day workweek has become one of the most talked-about workplace shifts of the last decade. Large corporations are experimenting with it....

We've all seen the headlines. Another major company announces that everyone needs to be back at their desk. No exceptions. And if you're running a...

If you work with a payroll provider for your small business, payroll typically runs on a set schedule with very little day-to-day involvement from...