Eric Joern

Eric Joern

How to Know If a Four-Day Workweek Is Right for Your Business

The four-day workweek has become one of the most talked-about workplace shifts of the last decade. Large corporations are experimenting with it....

It’s easy to want to skip to the "bottom line" of your financial statements, but like any great story, you’ll need context for the ending to make sense.

Your financial statements are THE keys to understanding what is going on with your company, but it’s more than that: they tell the story of your business. We get it, it’s fun to jump to the bottom of the page and look at your net income number because you want to know how much money you make.

The problem is that this only gives you a small sliver of the story of your business. The purpose of good financial statements is that they really tell the narrative of what your business has been doing over the time span that they cover. If you skip to the end of the story, you’re hamstringing your ability to enact meaningful change for your company. That can lead to losses in profits, missed opportunities, and other preventable mess ups that’ll make you feel upset and frustrated in hindsight.

So how do you read your financial statements? We’re glad you asked.

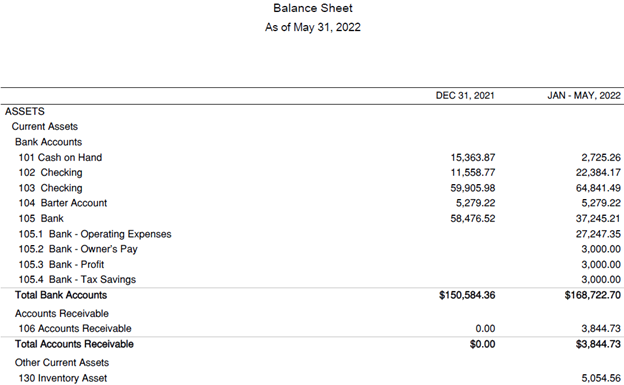

You can see in our example sheets that we’ve set up a comparative balance sheet from December 31st last year to May of this year. In this case, the client is up 18k in cash with another 4k owed to them in receivable money. Their inventory grew by 5k – which means a lot more inventory on hand.

We can also see that they have prepaid state replacement tax listed. That means they’re paying some tax ahead of time to cover the tax on the profit of the business. Basically, these are your assets. These are all liquid assets.

One thing to note: This hypothetical client also has several Profit First accounts set up. We highly recommend reading Profit First as a primer for understanding how to make the most of your business.

Fixed assets are basically physical, tangible items that your business has invested in. That could be money spent on things like leasehold improvements. In the case of our hypothetical client, they’ve erected a small structure on their property so it’s classified as a building.

We also have all the equipment, fencing, and other improvements they made in their shop. We want to figure out how much depreciation there has been on those new assets, so we’ll need to look at what they’ve taken in tax deductions vs what they’ve invested back into their business.

Here’s what we learn: they’re going to want to take some of their deductions in future years.

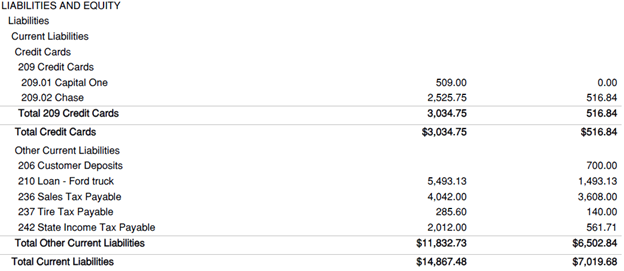

What can we learn from the liability section of this financial statement? Well, this business has cleaned up their credit card balances – from $3k down to just $500. They’ve also paid down the loan on a company vehicle. We can also see that they’ve been collecting sales tax throughout the month, so the collected tax from May 1st through May 31st, they’ll have to pay by June 20th. That means $3608 will have to be paid, and in most cases an accounting provider will schedule and file the sales tax return – but if they don’t have one, they’ll need to make sure they get that done on their own.

We can also see that there’s some long term liability. In this case, we see that they’re paying off a Ford truck this calendar year. That’s considered a current liability because that’s a debt you’re going to pay off in the next 12 months. More than a year would be considered a long term liability.

You’re probably aware of this, but you can loan your business money – in fact you probably WILL be loaning your business money the first few years. When you do that, you actually have to charge your own business interest on paying it back. So when we’re looking at a shareholder loan, that means the total amount that they did in that calendar year. In this case, our company was loaned 10k in the last calendar year and then another 19 on top of that the next year.

You can only deduct that interest once you pay it. That’s why you can see they have a holding account that is essentially the amount of interest that’s been accrued. They still haven’t paid themselves this interest yet, so that might be something to focus on in the future.

Finally, we arrive at the equity section. Most of the time, you think of equity as the difference between what something is worth and what you owe on it. On your balance sheet, it very much shows something similar — with one quirk. It does not account for the fair market value of your business' worth, but rather the "book" value of the business (what you paid, less the deductions you used on those assets).

In our example, the business owner kept profits from last year and current year profits, increasing their overall equity.

In this case, our financial statements shed a lot of light on where our business owner is currently. Their debt has gone up, but mostly because they infused more cash back into the business. That means that profits from prior years have been put back into the business to create a healthy bank balance.

In fact, it might be TOO much in the bank. Typically we want about three months' worth of emergency savings in the bank to cover expenses. We also saw that they’ve started their Profit First accounts to stay organized. We’d want to make sure all their bank accounts are squared. That said, we always like to keep it simple and process-oriented — the more money you’re moving around the more confusing you’re making it.

Ultimately, this business is in great shape and is positioned to plan for the future. That’s going to give them peace of mind in their day-to-day work on their business and unlock new opportunities, thanks to a better understanding of their full financial story. That’s the power of financial statements.

YPD HCM is part of the Kaizen CPAs family. YPD HCM specializes in payroll and HR compliance for small businesses, providing the hands-on support to get your people paid and stay compliant without having to become an expert yourself.

The information in this article is provided for general educational purposes and reflects conditions as of the publication date. It does not constitute legal, tax, or compliance advice. For guidance specific to your business, consult a qualified professional.

The four-day workweek has become one of the most talked-about workplace shifts of the last decade. Large corporations are experimenting with it....

We've all seen the headlines. Another major company announces that everyone needs to be back at their desk. No exceptions. And if you're running a...

If you work with a payroll provider for your small business, payroll typically runs on a set schedule with very little day-to-day involvement from...