Henry Joern

Henry Joern

Why Your Auto Repair Shop Needs a Business Coach to Grow

I played hockey growing up, and every team I was on had a coach. That coach never played in games. He wasn't scoring goals or making the big save....

Prices have gone up almost everywhere over the last few years. Groceries, gas, insurance, the parts and materials that go into whatever you make or sell. It's easy to feel that in your own wallet long before you sit down and think about what it means for your business.

The instinct for a lot of business owners is to raise prices "a little" and hope that covers it. But guessing at a number isn't a pricing strategy, it's a shot in the dark. Rising costs put every business in the same position: you need to respond, and the real work is figuring out how much to change and how to think it through so the change actually protects your business instead of just reacting to it.

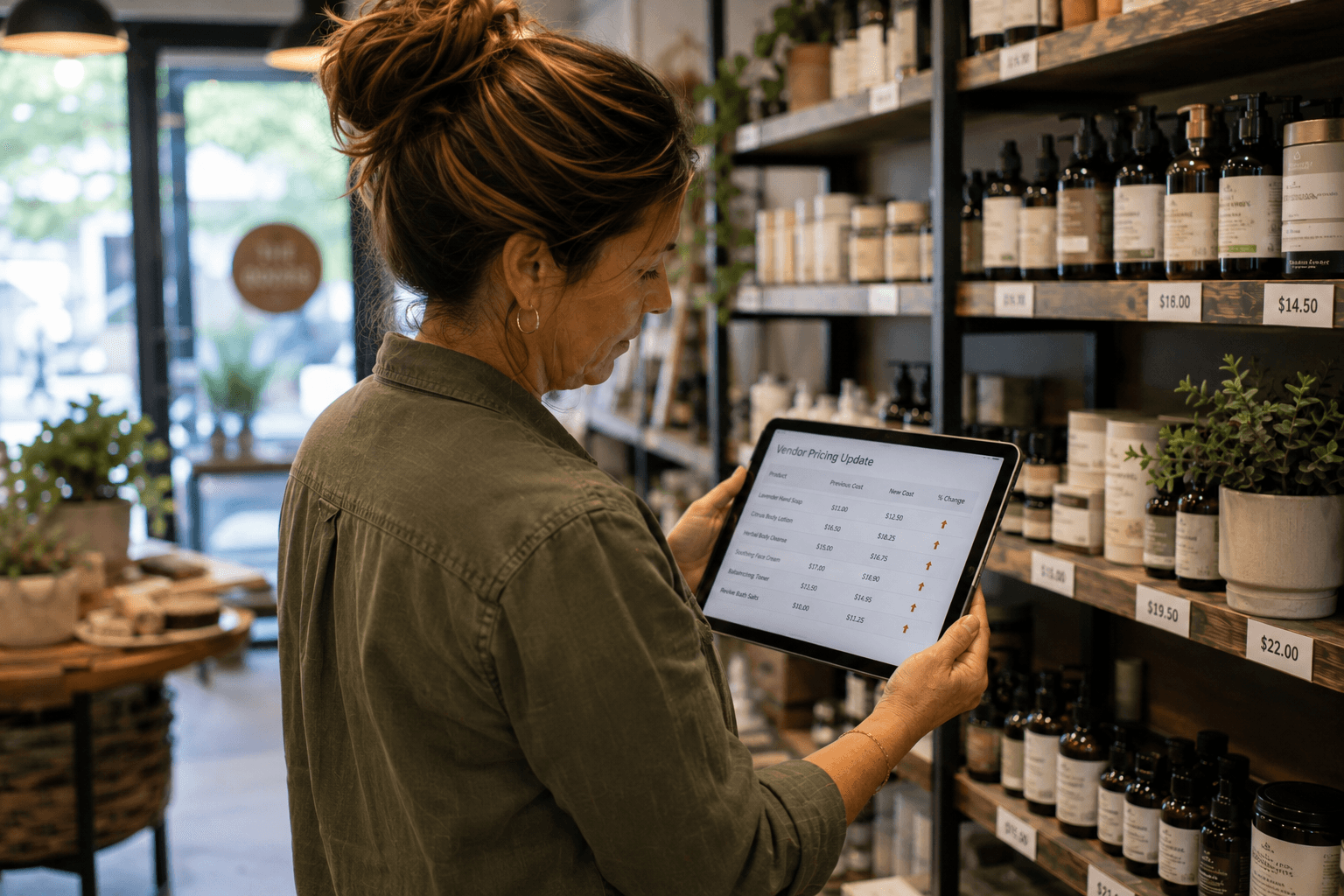

Cost increases rarely start with your business. They usually start further up the chain. Distributors pay more for raw materials. Vendors pay more for labor and transportation. At some point, those increases get passed down, and now you're paying more for the same things you were buying a year ago.

This isn't a new phenomenon, it's just more visible right now. Think about how much a fast food combo meal cost a decade ago compared to today. Prices that once felt fixed have moved dramatically over time, in some cases multiplying several times over, and people still buy the product. That's not an accident. Businesses raise prices because their own costs went up, and because employees and vendors are doing the same thing to support their own cost of living. It's less a single decision and more a chain reaction that eventually reaches your invoice.

Understanding that this is systemic, not personal, matters. It's not that your vendor is trying to squeeze you. It's that everyone in the chain is responding to the same pressure, and now it's your turn to decide how to respond to it.

Once a vendor increases their price, most business owners know a change is coming on their end too. The mistake is treating that change like a guess. "I'll probably bump it up a few bucks" feels reasonable in the moment, but it's not actually tied to anything. It doesn't tell you whether you're protecting your margin, eroding it, or accidentally overcorrecting.

The better question is what your pricing needs to do for your business. Are you trying to protect your gross margin percentage, or are you comfortable protecting a flat dollar amount per sale instead? That distinction matters more than people expect, and it's worth understanding the difference between markup and margin before you touch your price list. We've written more about that here: Markup vs. Profit Margin Explained.

The formula is simple: divide the amount your cost increased by the reciprocal of your target gross margin. That's the version that actually holds up under pressure, whether you're pricing one item or reworking a whole price list.

Say a vendor raises their price by $1, and your target gross margin is 50%. You'd divide that $1 increase by 50%, which comes out to $2. That's how much you need to raise your price to maintain the same margin percentage on that item. It feels like a bigger jump than "just passing along the dollar," but that's the point. If you only pass along the exact cost increase, your margin actually shrinks, because your fixed costs, overhead, and everything else on top of that item still need to be covered.

This same math applies whether you're pricing a part, a service, or a product line. It's simple enough to run in your head once you've done it a few times, and it removes the guesswork that leads to underpriced products six months down the road.

Most businesses default to the approach above: scale pricing with cost increases to protect margin. That's the safest starting point, and it's the right call for most situations.

But it's not the only strategy. Some businesses deliberately choose to hold their price increases below what the formula suggests, accepting a slightly lower margin per sale in exchange for higher volume. It's a strategy some large, high-volume retailers, like Walmart, are known for. The idea isn't to maximize margin on every transaction, it's to maximize volume while keeping fixed costs, overhead, and staffing relatively stable. It tends to work because scale allows for negotiating better costs from vendors in the first place, which offsets some of the margin given up on the front end.

This isn't the right move for every business, and it's not something to back into by accident. It only works as a deliberate strategy, paired with a clear understanding of your fixed costs and how much volume growth you'd actually need to make up the difference. If you're not intentionally choosing this path, the margin-based formula above is the safer default.

Raising prices is one lever. Reducing what it costs you to deliver the product or service in the first place is another, and it's worth exploring before you assume a price increase is the only option. That can mean renegotiating with vendors, reviewing your parts pricing structure, or finding ways to get more output from the same labor hours. If pricing parts is part of your business, this is worth a closer look: Pricing Parts in Auto Repair Shops, and if you want a more structured way to apply it, we also put together a Parts Pricing Matrix that can help.

Even a modest improvement in productivity, getting the same team to produce a bit more without adding headcount, can meaningfully offset the amount you'd otherwise need to raise prices. It's worth reviewing your processes every year regardless of whether costs are spiking, but it becomes especially valuable when they are.

A lot of business owners hesitate to raise prices because they're worried about conflict. Nobody enjoys the conversation where a customer pushes back on a price change. But in most cases, the pushback comes from a small, price-sensitive segment of your customer base, not the majority.

If you let that outlier group dictate your pricing, you're effectively letting the least profitable part of your business set the terms for all of it. That's not a sustainable way to run things. It doesn't mean you should ignore every customer concern, but it does mean the health of your business should carry more weight than the discomfort of a few difficult conversations.

The businesses that struggle most with rising costs usually aren't the ones that raised prices and lost a few customers. They're the ones that waited too long out of fear, and quietly bled margin every month in the meantime. The sooner you make the adjustment, the less profit you leave on the table waiting for a conversation you were going to have eventually anyway.

Pricing decisions like these don't just affect the invoice you send out, they affect your margin, your cash flow, and how the rest of your financial picture holds together.

If you're not sure whether your current pricing is actually protecting the margin you think it is, that's worth a closer look. We help business owners get proactive with financial planning and understand what their numbers are really telling them, before small pricing gaps turn into bigger problems. Book a call to see if we're a good fit.

Bulletproof Your Business and Thrive in a Recession

How Tariffs Impact Auto Repair Shops

EPA Responds to Trump's Freedom to Fix Memorandum

Shop Profit Leak Diagnostic (tool)

YPD HCM is part of the Kaizen CPAs family. YPD HCM specializes in payroll and HR compliance for small businesses, providing the hands-on support to get your people paid and stay compliant without having to become an expert yourself.

The information in this article is provided for general educational purposes and reflects conditions as of the publication date. It does not constitute legal, tax, or compliance advice. For guidance specific to your business, consult a qualified professional.

I played hockey growing up, and every team I was on had a coach. That coach never played in games. He wasn't scoring goals or making the big save....

Every business, including yours, moves through stages. Someone learns a skill, gets good enough to sell it, and at some point makes the leap from...

A lot of people ask me some version of the same question lately: is now still a good time to be in the auto repair business? The short answer is yes....